Buying your first home in Downriver Michigan means getting pre-approved with a local lender, choosing the right Downriver city for your commute and budget (Trenton, Riverview, Wyandotte, Southgate, Woodhaven, Grosse Ile, and Allen Park all trade differently), making a competitive offer with an experienced local agent, and completing inspection, appraisal, and closing — typically 30 to 45 days from accepted offer to keys in hand. If you're a first-time buyer looking at Downriver Detroit, this guide walks you through every step, with the Michigan-specific details national sites usually miss.

Quick answer: the 7-step first-time buyer path in Downriver MI

- Check your credit and save for down payment + closing costs

- Get a true pre-approval (not just pre-qualified) from a local lender

- Pick your Downriver target cities based on commute, schools, and price

- Tour homes with a local agent who knows Downriver — not a relocation call center

- Write a competitive offer (earnest money, contingencies, closing date)

- Complete inspection, appraisal, and final loan approval

- Sign at closing and get your keys

Most first-time buyers in Downriver close within 30–45 days of an accepted offer. The whole journey — from "I think I want to buy" to moving day — usually runs 2–6 months.

Step 1: Get pre-approved before you start touring homes

The #1 mistake first-time buyers make in Downriver is falling in love with a house before they know what they can actually afford. A pre-approval letter from a reputable local lender tells you three things:

- Your real purchase price ceiling

- Your likely monthly payment (principal, interest, taxes, insurance)

- How much cash you need at closing

Sellers in Downriver won't seriously consider an offer without a pre-approval letter attached. In a tight market like 2026, many won't even let you tour the home without one.

Pro tip: Get pre-approved by a local Michigan lender, not a 1-800 online lender. Local lenders know Downriver properties, Michigan's unique property tax rules, and can close faster when you're competing against other offers.

Step 2: Understand the Downriver Michigan market

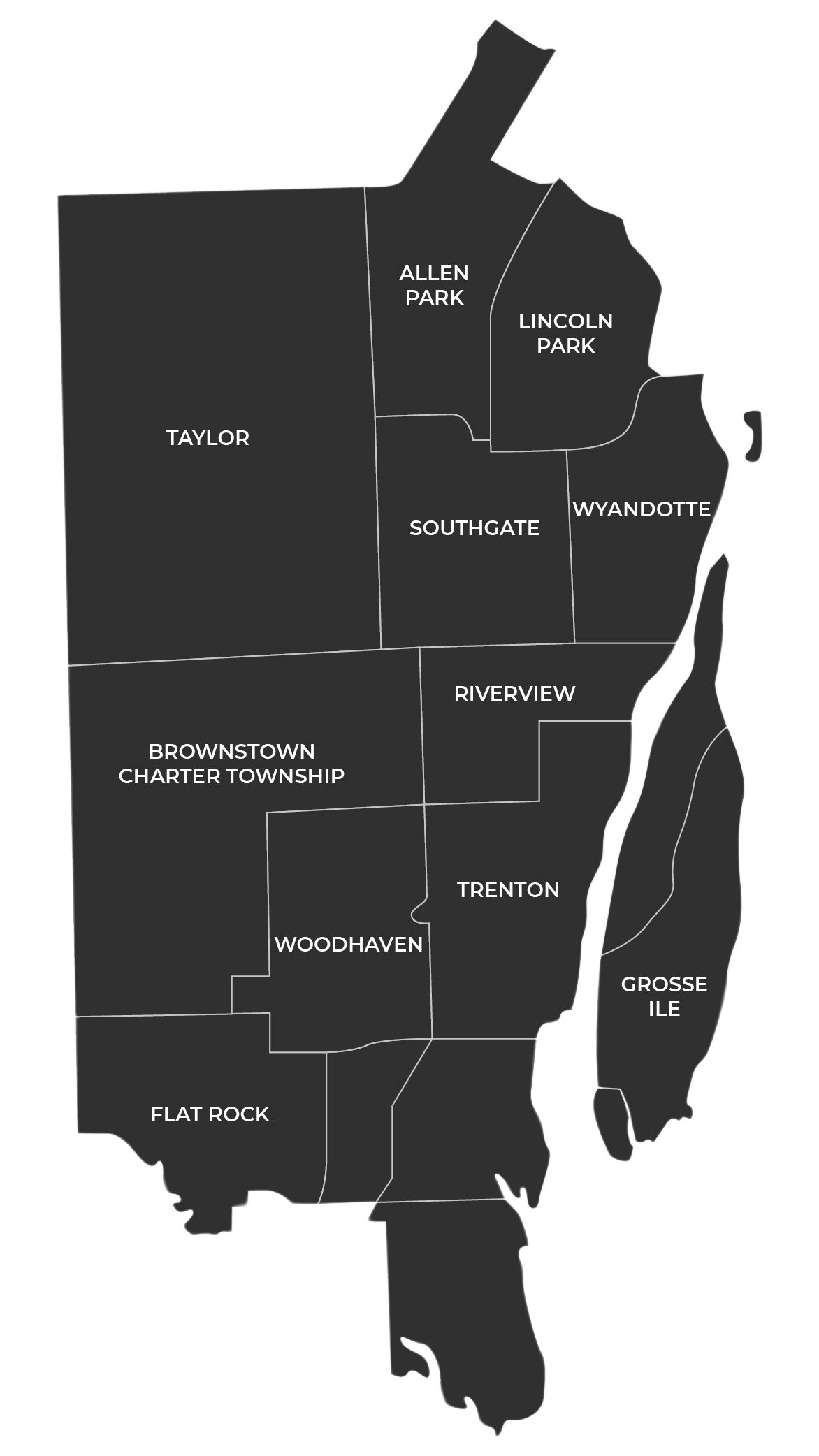

Downriver isn't one market — it's a cluster of small cities along the Detroit River, each with its own price point, school district, and character.

- Trenton — Waterfront town, strong schools, mix of mid-century ranches and newer builds. Median price ranges from the mid-$200s to $400K+ for Grosse Ile-adjacent homes.

- Riverview — Family-friendly, quieter streets, great value. Median sits in the low-to-mid $200s for a 3-bed.

- Wyandotte — Historic walkable downtown, bungalows, and brick Tudors. Popular with young buyers; $180K–$300K range.

- Southgate — Centrally located, ranch-heavy, close to shopping. Starter homes from $160K.

- Woodhaven — Newer builds, more cul-de-sacs, suburban feel. $250K–$400K.

- Grosse Ile — Island living, top-tier schools, waterfront premium. Entry point around $350K.

- Allen Park / Lincoln Park — Affordable entry, quick I-75 access to Detroit jobs. Starter homes from $140K.

First-time buyers in Downriver typically find their best value in Riverview, Wyandotte, Southgate, and parts of Allen Park.

Step 3: Pick the right Downriver city for YOU

Before you shop, nail down your non-negotiables:

- Commute — If you work in Detroit, Dearborn, or at one of the auto plants, your commute from Allen Park vs. Woodhaven can be 20+ minutes different.

- Schools — Grosse Ile and Trenton lead academically; Wyandotte and Riverview have strong community programs.

- Walkability — Wyandotte and downtown Trenton offer real walkable downtowns. Most other Downriver cities are car-dependent.

- Budget — See the ranges above; your pre-approval will narrow this fast.

- Home style — Ranch? Colonial? Waterfront? Each Downriver city has different housing stock.

Step 4: Tour homes — the right way

Hire a real estate agent who actually sells in Downriver, not a national referral service. A local agent will:

- Know which streets flood, which have the newer sewers, and which have HOA drama

- Know the listing agents and can get your offer seen quickly

- Have relationships with local inspectors, lenders, and title companies

- Spot red flags in a 1950s basement that a relocation agent would miss

Keep a short list. Don't tour 40 homes — tour 5–10 and make a decision.

Step 5: Write a winning offer

A Downriver offer in 2026 typically includes:

- Purchase price — Often at or above list in hot sub-markets

- Earnest money deposit — $1,000–$5,000 held by the title company

- Financing contingency — Protects you if the loan falls through

- Inspection contingency — Usually 5–10 days from acceptance

- Closing date — 30–45 days out is standard

- Appraisal contingency — Michigan default is yes; waive only if you can cover a gap in cash

Your agent will strategize with you based on how hot the specific property is. A well-priced Trenton ranch will often see multiple offers in the first weekend; a dated Allen Park colonial may sit for weeks.

Step 6: Inspection, appraisal, and final approval

Once your offer is accepted:

- Inspection (days 1–7) — Hire a licensed Michigan inspector. Expect to spend $400–$600. In Downriver, pay close attention to basements (moisture), roofs (hail damage is common), and older electrical.

- Appraisal (days 7–21) — Your lender orders this. If the appraisal comes in low, you and the seller will renegotiate.

- Final underwriting (days 14–30) — The lender verifies every document. Don't change jobs, open new credit cards, or make large purchases during this window.

Step 7: Closing day

Closing in Michigan happens at the title company. You'll bring:

- A cashier's check or wire for your closing funds

- A government-issued ID

- Your final loan documents (if not already signed electronically)

You'll sign about 40 pages. The seller signs. The title company records the deed. You get the keys. Most Downriver closings take 60–90 minutes.

Michigan-specific things every Downriver first-time buyer should know

- Principal Residence Exemption (PRE) — File this with your city within 90 days of closing. It can cut your property tax bill roughly in half.

- Summer vs. Winter taxes — Michigan bills property tax in two installments. Your escrow handles it, but you should understand it.

- Uncapping of taxable value — When a home sells, the taxable value resets. Your first year's property tax as the new owner will likely be higher than what the previous seller paid.

- Down payment assistance — MSHDA (Michigan State Housing Development Authority) offers first-time buyer programs with down payment help up to $10,000. Ask your lender if you qualify.

- Radon testing — Downriver Michigan is in an EPA Zone 2 radon zone. Get it tested during inspection; it's cheap and easy to mitigate.

How much money do you actually need to buy your first home in Downriver?

For a $225,000 home with 5% down, plan for roughly:

- Down payment: $11,250

- Closing costs: $5,500–$7,500 (lender fees, title, prepaid taxes and insurance)

- Inspection: $400–$600

- Moving + first-month utilities: $1,000–$3,000

- Reserves (lender may require 2 months of mortgage payments in the bank): ~$3,500

Total out-of-pocket: $21,000–$26,000 for a 5%-down scenario. Less with down payment assistance programs.

Frequently Asked Questions

How much do I need to make to buy a home in Downriver Michigan?

For a $225,000 home with typical Downriver taxes and 5% down, you generally need a household income around $55,000–$65,000, depending on your other monthly debts and credit score. Your lender will run the exact number in pre-approval.

What's the average down payment for a first-time buyer in Downriver?

Most first-time buyers in Downriver put down 3–5%. MSHDA and FHA programs allow as little as 3.5% down, and VA loans (for eligible veterans) require 0% down.

How long does it take to buy a home in Downriver Michigan?

From accepted offer to closing, 30–45 days is typical in Downriver. The full journey — deciding to buy, getting pre-approved, house hunting, and closing — usually runs 2–6 months for a first-time buyer.

Is Downriver Detroit a good place to buy a first home?

Downriver is one of the most affordable and accessible parts of metro Detroit for first-time buyers, with strong community schools, short commutes to Detroit jobs, and median prices well below the regional average. Trenton, Riverview, and Wyandotte consistently rank among the best-value first-home markets in southeast Michigan.

What credit score do I need to buy a house in Michigan?

Conventional loans typically require a 620+ credit score. FHA loans accept 580+ with 3.5% down, or 500+ with 10% down. USDA and VA loans have their own thresholds. Talk to a local lender to see what fits your situation.

Do I need a buyer's agent to buy a home in Downriver?

Yes — and a good local one. As of 2024, buyer-broker compensation is negotiated directly in the buyer agency agreement. A Downriver-experienced agent pays for themselves in negotiation, inspection insight, and closing coordination.

Ready to buy your first home in Downriver?

The Saward Team at eXp Realty has helped hundreds of first-time buyers close in Trenton, Riverview, Wyandotte, and the rest of Downriver Michigan. We'll walk you through every step — pre-approval to keys — and make sure you don't overpay or get burned by a bad inspection.

Call or text us at (734) 977-1405 or contact us through our website to get started. No pressure, no cold sales calls — just straight answers from agents who've done this hundreds of times.

Check out this article next